Trust & Estate Planning

How Physicians can Avoid Leaving Heirs a Giant Tax Bill

Published September 29, 2023

According to a rule instituted in 2020, non-spousal beneficiaries of retirement accounts now must draw down those savings within 10 years — often leaving them with a sizable tax bill. Below, we’ll take a look at what high earners are doing to amend their estate plans and what physicians should consider when leaving money to their children and grandchildren.

Understanding the 10-year rule

Prior to 2020, non-spousal beneficiaries who inherited a 401(k) and/or Traditional IRA accounts had a large window of opportunity to withdraw the pre-tax funds in those accounts. Since the Secure Act was passed, however, these beneficiaries have just 10 years from the death of the original account holder to draw down those funds.

For child beneficiaries of Traditional IRAs and 401(k) accounts, this 10-year rule comes into effect once they become “majority age,” which ranges between 18 and 21 years of age depending on what state they live in.

The new rule is part of several recent changes to the tax code aimed at preventing some savers from sheltering pre-tax money over long periods of time. Now, taxes on these pre-tax savings must be paid soon after the death of the original saver — putting more pressure on beneficiaries to pay them over a shorter period of time.

On top of this, there are stringent restrictions on what beneficiaries can do with inherited IRAs. For instance, they can’t be converted to a Roth IRA after the death of original owner — nor can beneficiaries add their own money to inherited IRAs. In most cases, non-spousal beneficiaries are legally obligated to simply withdraw inherited IRA funds over that 10-year period and pay taxes on any of the savings that were deposited on a pre-tax basis.

As the Wall Street Journal recently reported, the Secure Act has many savers revising their estate plans to avoid this scenario and instead leave non-spousal beneficiaries with Roth savings. In these cases, grandparents are converting their pre-tax accounts into Roth accounts, essentially pre-paying the taxes on the savings so children and grandchildren won’t have to. In most cases, Roth IRA beneficiaries are subject to the same 10-year rule, but beneficiaries can leave the money to grow over that time and one bulk withdrawal in the 10th year will be tax-free.

The estate planning benefits of Roth IRAs

Beyond their usual benefits (tax-free growth of savings, tax-free withdrawals, no required minimum distributions, etc.) there’s another key reason why Roth IRAs are so advantageous to estate planning and beneficiaries: easy transfer of ownership.

Roth IRA savers essentially have two options to pass down their after-tax money. The first option is leaving the funds in the Roth IRA to heirs. In this case, the estate executor pays out the money according to the owner’s will, resolves any applicable taxes, and closes the Roth IRA. Beneficiaries in this scenario receive a lump sum to invest, save, or spend as they see fit.

The second option is to name the non-spousal heir as the Roth IRA beneficiary on the account itself. Most retirement accounts allow you to name a beneficiary and the Roth IRA is no different. Naming a beneficiary on the account (rather than in a will) means that beneficiaries immediately assume ownership of the Roth IRA when the original owner passes away.

Roth IRAs with named beneficiaries avoid the probate process and most inheritance taxes. That means beneficiaries don’t have to wait for probate to be completed before receiving the money — transfer of ownership occurs quickly and with fewer expenses. For larger estates, however, Roth IRAs will still be subject to an estate tax, even when there is a named beneficiary on the account.

If you’re a physician who has concerns about how your assets will be passed down to beneficiaries, Earned is ready to assist you. Our experienced financial advisors specialize in physician wealth management and can help tailor your estate plan so that taxes are minimized and loved ones are taken care of. Contact our team today to get started.

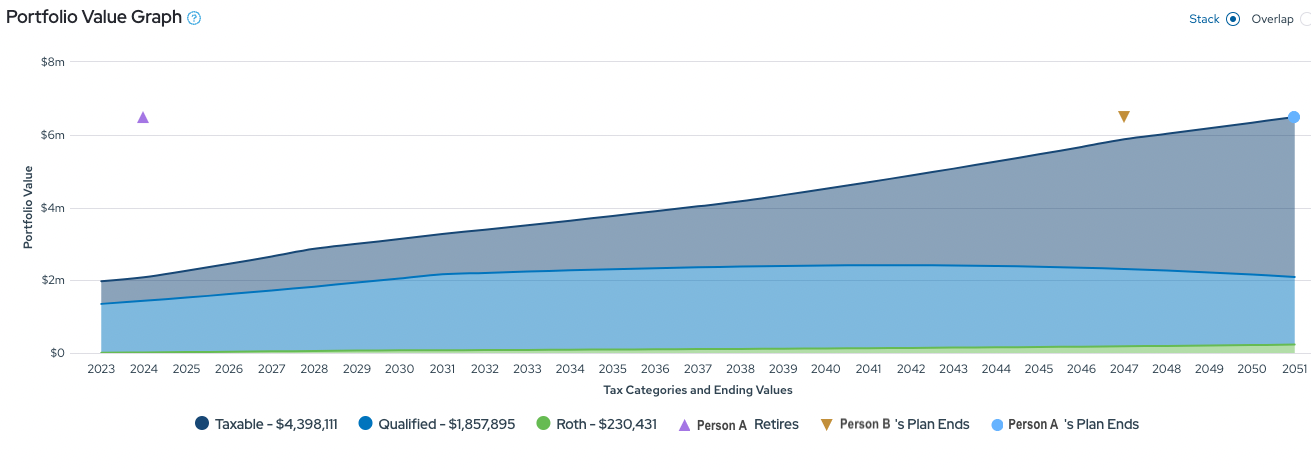

Case study: The power of Roth savings

For more and more physicians, Roth savings are emerging as a critical part of their portfolio, both in terms of retirement saving and estate planning. The graph above shows the projected portfolio of one Earned client looking to maximize their retirement savings.

You can see a substantial qualified (employer-sponsored) account alongside an even more substantial taxable account in the blue and gray areas. As discussed above, passing these tax deferred accounts down to beneficiaries can result in significant tax liability because of the 10-year rule. The Roth savings, in green, are positioned for minimal growth in this forecast.

In fact, this income tax liability significantly diminishes the actual value of the 1.8 million dollar qualified account, making it less valuable than it may initially appear. Additionally, this scenario could potentially push the beneficiary into a higher tax bracket than they might normally find themselves in.

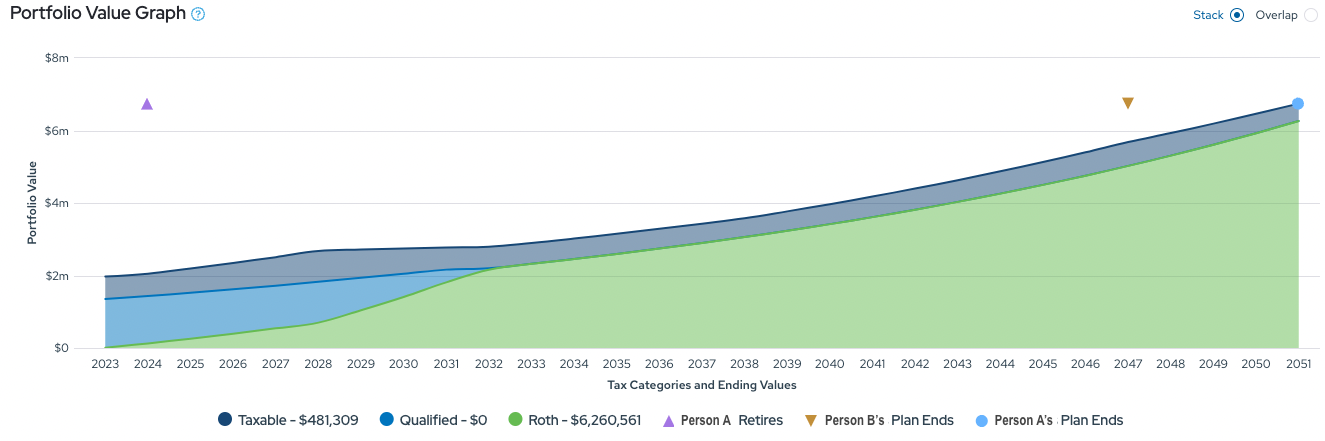

In this second chart, Earned projects the client’s portfolio value with recommended Roth conversions strategized by an Earned advisor. The qualified account is depleted earlier in retirement, while the Roth account continues to grow and becomes the primary component of their assets.

As discussed earlier, any heirs inheriting this portfolio can continue to let the Roth savings grow for another 10 years and then receive a lump sum without incurring any tax liabilities. Both of these charts pertain to the same client, but there's a crucial difference: Earned executed Roth IRA conversions for the client during the optimal period (at the beginning of retirement when their income and tax rates were lower).

This strategic move ensures that by the time they reach the age of 73, when required minimum distributions (RMDs) would typically apply, there are no RMDs. As a result, we can maintain the client and their spouse in a lower tax bracket throughout their retirement.

How Earned can help

Estate planning is a sensitive but essential process to wealth management. As illustrated above, Earned has helped physicians and their spouses grow their assets not only for themselves and their retirement, but also for eventual beneficiaries of their estate. With a vigilant eye on reducing unnecessary tax drag on earnings and investments, Earned has helped our clients reach their retirement and estate planning goals — all while eliminating the stress of financial management.

If you’re a physician with concerns about maximizing your retirement savings and positioning those assets to best benefit your eventual heirs, our experienced advisors are ready to help. Contact Earned today to schedule a complimentary consultation with our team.

Earned Wealth (a DBA of NoHo Financial, Inc) is an SEC-registered investment adviser located in New York City, NY. Registration as an investment adviser does not imply a certain level of skill or training.Earned Wealth's website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publication, and links. All examples are for illustrative purposes only and may not be relied upon for investment decisions. The publication of Earned Wealth's website on the Internet should not be construed by any consumer and/or prospective client as Earned Wealth's solicitation or attempt to effect transactions in securities, or the rendering of personalized investment advice over the Internet.A copy of Earned Wealth's current written disclosure statement as set forth on Form ADV, discussing Earned Wealth's business operations, services, and fees is available from Earned Wealth upon written request. Additional Information about Earned Wealth and our advisors is also available online at https://adviserinfo.sec.gov/.Earned Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.Investing involves market risk, including possible loss of principal and investment objectives are not guaranteed.

![]()

![]()

![]()

![]()

© 2024 Noho Financial Inc

30 Cooper Square, 10th Floor, New York, NY 10003

Investment advisory services offered through Earned Wealth, an SEC-registered investment adviser.